Taking a Moment

There’s a lot that goes into the production of a Weekly Roundup that many readers don’t see. Looking back on the week that was is as much a habit as knowing which letters to capitalize in an online brokerage’s name. Despite the hundreds of times having done this, occasionally something happens in a week that forces a pause from business as usual.

This past week there was a terrible tragedy that took place in London, Ontario. Four members of a family were murdered simply for looking and being different than what someone decided was appropriately Canadian. They were murdered because they were Muslim.

Like many Canadians, it is hard to find words to capture how thoroughly awful and traumatic this event was. And so, we are left with yet another heavy but necessary exercise: to not turn away from the terrible news but this time to watch and engage.

The news cycle will move on before the people will. A young boy will be left to figure out the rest of his life without his parents and sister beside him. Muslims and other religious and ethnic communities across Canada will forever be slightly less trusting that everything will be OK.

Before getting back to business as usual, I wanted to call attention to Islamophobia and the responsibility all of us bear to call out prejudice when and where we see it.

Please take a moment and either watch or read about this family.

All of us have a part to play in looking out for each other.

This mural was made by 15 year old Yumna Afzaal. Her star was stolen by hate but the spirit of her inspiring words cannot be denied. It should be shared & never forgotten. This is what every Canadian should aspire to #OurLondonFamily pic.twitter.com/aAYF9bKpw0

— Abdu Sharkawy (@SharkawyMD) June 8, 2021

A Tale of Two Tables: 2021 MoneySense Online Brokerage Rankings Released

It’s hard to believe, but the DIY investor datapalooza (or datastravaganza?) that is characterizing 2021 continues to chug along well into June.

Earlier this month, a popular Canadian investment publication, MoneySense magazine, published their 2021 Canadian online brokerage rankings, essentially capping off the last of the major discount broker rankings for the summer.

Even though the fall feels far away, online brokerages are undoubtedly at work planning for their ramp up at the end of the year. These latest Canadian online brokerage rankings will ultimately prove to be a big part of what will help online investors shape their perceptions and decisions around which online broker they choose to go with, and ultimately impact how online brokerages market and talk about themselves for the rest of the year.

Why is this Online Brokerage Ranking Important?

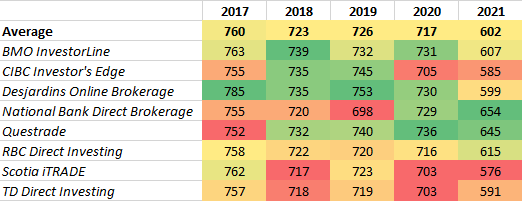

Now in its ninth year, the MoneySense rankings have become a go-to resource for many DIY investors curious about the online brokerage marketplace in Canada. As the landscape evolves for online brokerages and self-directed investing, so too do these rankings.

Helping MoneySense stay on top of those changes is Surviscor, a financial services research firm that evaluates Canadian online brokerages across a number of different parameters.

Frequent readers of the Weekly Roundup will already be familiar with the research and in particular, the online brokerage rankings, produced by Surviscor. For a timely throwback, be sure to check out our Look Back/Look Ahead series featuring Glenn LaCoste, President and CEO of Surviscor, and the author of this year’s MoneySense online brokerage rankings.

With yet another online brokerage ranking appearing this year, it’s a lot for online investors to digest. The MoneySense rankings in particular offer an interesting way to see the importance of defining what’s “best” when it comes to online brokerages. Also, in digging through the data, we uncovered an interesting relationship between a major driver of investor decision making, cost of services, and the performance on measures of investor experience – like service.

There’s lots to dig into, so grab some caffeine and get ready to scroll.

Methodology

Online brokerage rankings and evaluations help to make sense of the often-confusing question: “which online brokerage is best?”

With several Canadian online brokerage rankings available for online investors to consult, it is important to come back to a familiar concept – that each online brokerage ranking measures the idea of what’s best in a different way.

The MoneySense online brokerage rankings are often cited as a resource to evaluate almost all of Canada’s online brokerages. Like most of the other comprehensive rankings, information is published annually, and as a result, the data takes a snapshot of the past year or so in the world of DIY investing at Canadian online brokerages.

It is important to note that the data for the MoneySense online brokerage rankings comes from financial services research firm Surviscor. Specifically, according to the methodology, the MoneySense rankings are based on a combination of the following Surviscor reviews:

1. Online experience

2. Mobile experience

3. Cost of services experience

4. Service experiences

Points were assigned to each online brokerage according to a points-based system in which each brokerage received a score based on its ranking within the seven sections of the review:

1st = 5 points

2nd = 4 points

3rd = 3 points

4th = 2 points

5th = 1 point

The overall score was the sum of the awarded sections and reported as points.

In addition to reporting on the points earned by each brokerage as part of this review, the MoneySense rankings also reported the “Best online brokers” by category. The breakdown is as follows:

- Best online broker for fees

- Best online broker for customer service

- Best online broker for ETF investing

- Best online broker for stock investing

- Best online broker for financial literacy

- Best online broker for market data

- Best online broker for customer onboarding

- Best online broker for mobile experience

Within each of these categories, the top two firms were reported.

Strengths & Limitations

One of the strengths of the review is that there is lots of data reported for investors to consider, and it has been published in a way that identifies the top two firms in each of the stated categories. This saves a lot of time for investors or readers who simply want or need a quick answer from a reputable source.

A big plus this year is that there is a companion publication on the Surviscor blog which dives into detail on the scores and provides more context on the process.

In terms of limitations, presenting this volume of information can be a challenge. For example, the methodology stated:

“Each firm was assigned a score based on its ranking within the seven sections of review (5 points for first; 4 for second; 3 for third; 2 for fourth; and 1 for fifth), and the overall score was the sum of the awarded sections.”

Given that there are eight reported categories (noted above), it was not immediately clear which seven sections of the review were being referred to, and as a result, validating the math or seeing how scores varied across sections would have added important context to rankings.

For example, one of the immediate questions that jumps to mind with the points system is what the maximum possible score would be? Without that information, it is hard for the reader to get a sense of just how good a particular brokerage is. And, when the scores are close, or tied, the value of points and how they get calculated becomes even more important to contextualize results.

Results

The results for the 2021 MoneySense online brokerage rankings are shown in the following table.

| Firm | MoneySense Points | MoneySense Rank |

| Questrade | 36 | 1 |

| National Bank Direct Brokerage | 31 | 2 |

| TD Direct Investing | 25 | 3 |

| Qtrade Direct Investing | 22 | 4 |

| BMO InvestorLine | 9 | 5 |

| Scotia iTRADE | 6 | 6 |

| RBC Direct Investing | 5 | 7 |

| Desjardins Online Brokerage | 4 | 8 |

| Wealthsimple Trade | 4 | 8 |

| Virtual Brokers | 4 | 8 |

| Canaccord Genuity Direct | 4 | 8 |

| CIBC Investor’s Edge | 2 | 12 |

| HSBC InvestDirect | 1 | 13 |

| Laurentian Bank Discount Brokerage | 0 | 14 |

Questrade took the top spot in this year’s rankings with a total of 36 points, followed closely by National Bank Direct Brokerage (31 points), and TD Direct Investing in third place (with 25 points). Again, without a maximum score, it is difficult to know exactly how well any one brokerage could have done.

The methodology states that there are seven “sections” and a five-point maximum which would imply a maximum score of 35. However, Questrade has clearly exceeded that score, hence some confusion.

Data outside of the top five brokerages was not published in the MoneySense rankings, however, it was available on the Surviscor site, which helped identify additional context on how the entire field of online brokerages performed this year.

One of the first noteworthy items is just how sharp the drop off is from fourth to fifth place in these rankings. Qtrade Direct Investing placed fourth with 22 points. However, BMO InvestorLine, with just nine points, managed to make it into the top five.

Even though on a relative basis, a top five finish may not sound so bad, in the case of this year’s ranking, the distance between fourth and fifth is materially different.

Another interesting observation about the data is the number of firms who tied for eighth place. CG Direct, Desjardins Online Brokerage, Virtual Brokers, and Wealthsimple Trade are very, very different firms, and yet each tied for eighth place with four points.

Somewhat stunning are the positions of CIBC Investor’s Edge and HSBC InvestDirect, who placed 12th and 13th respectively. In the case of the former, being a “Big Five” bank-owned brokerage should in theory enable it to have the resources to score better, but with a score of two points, it implies that Investor’s Edge was rarely a top five brokerage in any of the evaluated categories. Similarly, HSBC InvestDirect scored one point, and it too barely placed in a top five finish in any of the categories measured.

Surviscor’s “behind the scenes” look at the MoneySense rankings also provided some additional context and important takeaways when it came to this year’s analysis. The following five statements were made in reference to the data and the items that online investors (and online brokerages) should pay attention to.

- Beware the marketing when it comes to fees

- Firms never get a second chance to make a first impression

- Financial literacy is weak

- Mobile experience is still not where it needs to be

- $0 commission is not always worth it

With so much data to crunch, it can be a challenge for DIY investors and industry analysts alike to form a “big picture” of what’s going on in the online brokerage space.

Surviscor’s multiple studies to measure online brokerages got us curious, so we compiled the ranking data from each of the four online brokerage analyses cited in the MoneySense rankings, and crunched the numbers to see what the correlation would be between the combined rankings of each evaluation and the MoneySense ranking data.

Methodology, Part Deux

First a(nother) note on methodology. The rankings in each of the four different Surviscor evaluations used in the MoneySense ranking were averaged out and reported along with a standard deviation. The computed rank is one that we generated based on the average rank across each of the evaluations.

To try and get as close to an apples-to-apples comparison of how different online brokerages ranked against each other in each of the four evaluations, it was necessary to make some minor adjustments to the data.

In the Service Experiences, Interactive Brokers was actually evaluated, so for the sake of consistency across comparisons, they were excluded from the data and the ranks of other brokerages adjusted upwards by one. Wealthsimple Trade was assigned the lowest value for not having been able to be measured. For the actual service experience scores, check the link here.

Adjustments were also made in the Online Experience and Mobile Experience rankings. Laurentian Bank Discount Brokerage and CG Direct were assigned the lowest rank since they did not offer anything that could be evaluated using those tools.

Results

One of the first things to stand out is that the top four brokerages in the 2021 MoneySense online brokerage rankings are the same four online brokerages when computing scores across the four Surviscor evaluations, however, the order in which they appear is different.

In the computed rank, the measure that we calculated, Qtrade Direct Investing came in first, followed by National Bank Direct Brokerage, Questrade, and TD Direct Investing, respectively. What also stood out in the top three is that the average rank between Qtrade Direct Investing, National Bank Direct Brokerage, and Questrade is very close, ranging between 4.0 and 4.8. Having the standard deviation handy (shout out to the stats profs who drove home the point about standard deviations) as a measure of consistency, however, adds a bit more nuance to the top three online brokerages.

Specifically, Qtrade Direct Investing has a relatively low standard deviation (2.3) indicating their ranking is relatively consistent from one evaluation to the next. By comparison, Questrade has the highest standard deviation of the group (5.7), which points to the remarkably poor ranking they received in the Cost of Services evaluation (they ranked 13th). Having the context of all the data helps to illustrate where exactly the top three online brokerages excel relative to each other, and to see how consistently (or inconsistently) online brokerages are scoring.

Consistency cuts both ways, however.

RBC Direct Investing had the lowest standard deviation (1.2) of all of the rankings, implying a fairly consistent score across different evaluation studies. Their average rank was sixth, and the computed rank put them in fifth place overall.

By comparison, Virtual Brokers also had a very low standard deviation score (relatively speaking) at 2.1, but their average rank of 9.8 landed them with a computed rank of 13th overall. This implies that Virtual Brokers has consistently performed poorly on the four Surviscor evaluations for 2021.

It was also intriguing to note that after about eighth place in the MoneySense ranking, the divergence between these scores and the computed rank became more pronounced. In particular, CIBC Investor’s Edge ranked 12th in the MoneySense ranking but ninth in the computed ranking, only slightly behind Scotia iTRADE and Desjardins Online Brokerage.

Takeaways

Being able to step back and take a big picture view of the data provides a unique window into how the different evaluations generated by Surviscor come together, and how they compare to the MoneySense rankings.

When placed side by side, the combined Surviscor studies used in the MoneySense ranking show that firms that are strong on experiential factors, such as online, mobile, and service, tended to do better overall in the rankings.

Interestingly, with the exception of National Bank Direct Brokerage, firms that tended to do well on pricing had a negative correlation to performance on the MoneySense or combined Surviscor rankings. This points out that perhaps there is an inverse relationship between the cost of services and the experience of online investing.

Thus, having the additional data presented in a big picture format does help illustrate what exactly online investors would have to trade off. For example, in choosing between Questrade and National Bank Direct Brokerage, investors can see that the tradeoff might be one of “cost of services” versus “online experience.”

Clearly there is lots of data to explore, which can be both a pro and a con for online investors looking for a quick answer to “which online brokerage is best?”

The reality is that rankings help to compress a lot of the analysis into an easy to digest number. However, as illustrated above, how one defines “best” – even when using the same underlying data – can impact how specific brokerages are perceived and reported on by media, online brokerages themselves, and other DIY investors.

What is evident in looking at the big picture of this data is that the field of Canadian online brokerages is crowded, and with even more new entrants poised to add to the numbers, keeping on top of the evolving space is an ongoing challenge. For those that want to avoid the spreadsheets and comparisons, rankings offer a quick shortcut. But like everything else when it comes to investing online, it pays to do your homework.

Into the Close

That’s a wrap on this week’s Roundup. It’s been a difficult week but here’s hoping we can look for, find, and create the good in the week ahead.

At the London multi-faith march to end hatred.

— Omar Sachedina (@omarsachedina) June 11, 2021

One marcher just told me: “We are seeing the best of humanity after seeing the worst.”#onelondonfamily pic.twitter.com/TNq4klaJyI