With summer just around the corner, it looks like stock markets won’t be the only ones seeing red. Weeks of volatility and sell-offs have been difficult for all but the most seasoned self-directed investors to stomach.

For DIY investors, the news isn’t all bad though. The pullback in stock markets typically means that online brokerages will need to work harder to encourage online investors to open an online trading account, and that means potentially bigger or more attractive incentives.

Although there aren’t any new deals that have launched at the start of the month, leading into June there have been several noteworthy developments in the online brokerage deals and promotions section.

By far, the biggest development last month was the launch of commission-free trading on stocks and ETFs at CIBC Investor’s Edge. This is huge news for younger investors, as well as for competing online brokerages across the board. As the first of the big five bank-owned online brokerages to offer full commission-free trading, it seems like CIBC’s peers will have to consider adjusting their commission rates or young investor offerings.

Fortunately for RBC Direct Investing, their 100 commission-free trade offer is both large enough and long enough in duration to weather this price move by CIBC Investor’s Edge. Perhaps it was fortuitous timing that RBC chose to extend their offer at the beginning of last month, and with this move from CIBC Investor’s Edge, they may consider extending it even further.

There’s no question that the list of commission-free online trading options is growing. TD Direct Investing, via their Easy Trade app, offers 50 commission-free stock trades per year, and National Bank Direct Brokerage and Desjardins Online Brokerage each offer full commission-free trading to investors of all ages. Of course, there’s still Wealthsimple Trade in the mix too.

Against that backdrop, the launch last month by Qtrade Direct Investing of a 50 commission-free trade offer does provide something to online investors looking for a deal when opening an online account, but clearly, the stakes have been raised.

The reality for Canadian online brokerages is that there are only a few months left to make plans for the next RRSP season, and with all the action happening in markets right now, for better or worse, online investors are checking their accounts and wondering if they’re getting great value. It’s one thing to sell a stock into a storm and another to incur a commission charge on a loss.

Expired Deals

Wealthsimple Trade’s “free stock” promotion expired on May 31st. This popular promotion has been a windfall for the zero-commission broker, mirroring the performance of US online brokerage, Robinhood, who has a similar (but actually a free stock) program in place.

Another important expired deal was from National Bank Direct Brokerage. Their recent promotional discount on margin rates seemed especially well-timed given the discussion on rising interest rates that is dominating the news cycle right now. It was the first “discount” on margin interest rates we’ve seen in some time, so given the current interest rate environment and volatility in markets, it could make this offer especially attractive to very active or sophisticated investors.

Extended Deals

Nothing new to report on this month as far as deal extensions are concerned. The RBC Direct Investing commission-free trade offer is worth watching as it was extended into this month.

New Deals

No new deals activity to report at the start of the month.

The budget and rate hikes have generated a lot of “interest” lately. Interestingly (see what I did there), the link between the discussion on frothy real estate and self-directed investing is a lot closer than you think, especially for one bank owned online brokerage.

In this edition of the Roundup, we review a fascinating set of data points to emerge around bank-owned brokerage Scotia iTRADE and explore what this remarkably quiet online brokerage is working on this year, as well as what peer firms and self-directed investors can learn from iTRADE’s recent activities. Also in the Roundup, an exciting upcoming webinar about getting into self-directed investing (featuring an expert panel that includes Sparx!). We close out this edition with a very timely selection of investor forum posts talking about iTRADE.

Whatcha Say Scotia iTRADE? A Deep Dive into Emerging Developments

We often spend time in the Roundup profiling Canadian online brokerages that are actively talking about new features. There are times, however, when it is warranted to pay attention to who is not speaking up about what they’re doing – especially when they are a bank-owned online brokerage.

Earlier this year, we published the latest edition of our Look Back / Look Ahead series, which offered leaders at Canadian online brokerages the opportunity to directly communicate what they’re working on to self-directed investors and industry enthusiasts alike. There was no charge to participate and all online brokerages in Canada were invited to submit a recap of what they were working on and what self-directed investors could look forward to in the year ahead.

Among the group of online brokerages that we did not receive a direct update about, Scotia iTRADE stands out as an interesting case, especially considering recent remarks from a pair of important conferences, notably the National Bank Financial Services Conference and the Scotiabank Annual General Meeting (AGM). Despite not receiving a direct update in the Look Back / Look Ahead, comments from these conferences have provided some clues as to what this online brokerage is focusing on for 2022, as well as their strategy when it comes to competing in the current online brokerage marketplace.

DI-Why Investors?

Often, communications by financial services firms are vetted and polished through numerous steps before they get released into the real world. Occasionally, however, things slip through the cracks. Recently, we were able to get a bit of a hot take on the world of self-directed investing, in particular, of younger investors from Scotiabank.

The comment, which came from Scotiabank’s Group Head, Canadian Banking, Dan Rees, was as follows:

So, younger individuals who don’t want to take advice and want to go DIY on their own. Generally speaking, those don’t work out that well, right? That said, we also know that we have sophisticated investors who do want to run their own money as part of managing their overall portfolio, so they may have a relationship with a portfolio manager and run 15% on their own, in our case in an iTRADE account. And we want to support both of those positions.

There’s a lot to unpack from that statement; however, the focus for Scotiabank, it seems, is on servicing sophisticated clients (read: high net worth) with advice-related products rather than the self-directed investing products. Since younger investors don’t typically fall into that category, these remarks imply that resources will be prioritized for sophisticated self-directed investors rather than entry point ones. This is especially interesting considering several peer bank-owned online brokerages are paying much more attention to supporting new retail investors.

As if to make very clear where Scotia is directing their attention, the image on the Scotia iTRADE homepage also skews directly towards “homeowners” rather than those whom would not have a mortgage (or own their own home).

Mr. Rees’s comments seem to explain a lot when it comes to the curious silence and muted online presence that Scotia iTRADE has had for several years now.

Whereas previously Scotia iTRADE was active on social media and in promotions, investor education, and platform enhancements, these seem to have all been dialed back considerably. But based on some comments at another conference, that might soon change – at least when it comes to technology.

The other interesting place where Scotiabank talked openly about Scotia iTRADE recently was at the Scotiabank AGM early in April. Normally, an AGM is not really the forum to air grievances about the online brokerage experience. So, it was both surprising and telling to see that the first question raised at the Scotiabank AGM came from a Scotia iTRADE client (and Scotiabank shareholder) Robert Wells. And this time, the “official response” sounded a lot more official.

Mr. Wells’ question was as follows:

Scotia iTRADE charges me $270 to enter and exit a $500 options trade and competitor banks only charge $40 for the same trade and it is disconcerting for a shareholder to feel compelled to transfer my brokerage account to another bank that charges almost 1% less for margin loans, far less on fees and commissions and provides far better customer service. Does Scotiabank management have an estimate of how many other customers are transferring their accounts to no or low commission banks? And, does Scotiabank management have a strategy to remain competitive in this new era of low fee brokerages?

The response from Senior Vice President Client Solutions and Direct Investing, Erin Griffiths:

At Scotiabank we strive to deliver a consistent high-quality experience across our platform and at Scotia iTRADE specifically we review our fee schedules regularly to ensure they are competitive in the Canadian marketplace, that they are compliant with the local regulatory framework, and also that they are delivering value to our clients.

For the option trading specifically, we charge $1.25 per contract which is consistent with many of our peers and we also offer free trading through the Scotiabank Ultimate Banking package as well as through over 100 different exchange traded funds that we have on our platform.

With regards to value, we’ve invested significantly and continued to invest significantly in our people and our platform. We have increased our contact centre staffing by 32% over the past year, and we continue to invest also in our technology, modernizing the online experience for our clients; launching a new mobile application later this summer and a new active trading platform later this year in addition to many other things.

And then finally with regards to the question around transfer out activity, we regularly monitor that on a monthly basis, and we are very pleased to see that consistently we have more clients who transfer into iTRADE as their platform of choice over transferring out, and that has allowed us to continue to increase our market share and assets relative to our peers and add shareholder value.

There’s a lot of information provided in both the question and the response; however, it is clear that just because Scotia iTRADE doesn’t talk much about what they’re working on, it doesn’t stop people – including shareholders – from wondering what they’re doing, especially in this ultra-competitive segment (see the From the Forums section below for more examples of this). It’s also clear that things are being worked on at Scotia iTRADE, just not being telegraphed well to broader stakeholders.

Customer Sad-is-fact-ion

What shines through loud and clear from the question by Mr. Wells is the dissatisfaction with commission pricing, margin fees, as well as customer service.

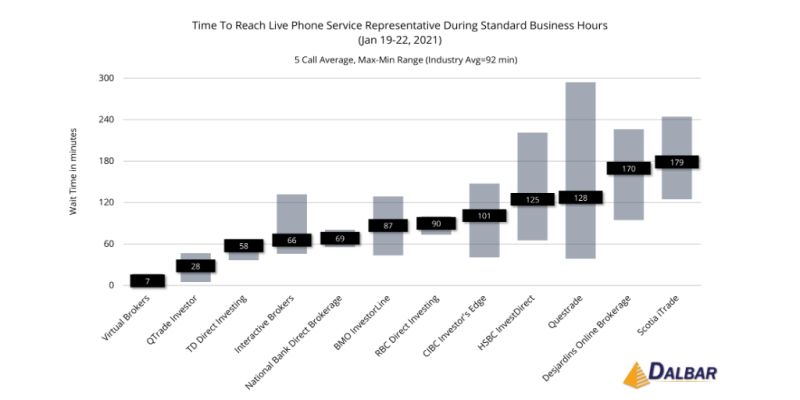

Any regular reader of the Roundup will know that Scotia iTRADE has struggled with meeting customer service needs over the past few years. So although it is a surprise to see a question about service levels surface at an AGM, it is certainly not a surprise to hear this being an issue that clients of Scotia iTRADE experience. Of course, what “better customer service” means exactly is up for debate, but there are at least three different ranking firms that paint a consistent picture of Scotia iTRADE falling short when it comes to delighting clients.

Last year, for example, DALBAR Canada, which regularly reviews phone and chat service at Canadian online brokerages, found Scotia iTRADE had an average phone wait time of 179 minutes – the longest average phone wait time of all brokerages surveyed. And although their survey was taken at a time when volumes were actually higher than normal in 2021, it speaks to the responsiveness and preparedness of call centres to handle the needs of clients that end up having to call in.

Surviscor, another firm which analyzes the Canadian online brokerage marketplace, found that Scotia iTRADE averaged 64 hours to respond to service inquiries by email, according to the latest Surviscor ratings of iTRADE. Despite the service experience, however, the overall ranking for Scotia iTRADE was still reasonably high according to Surviscor, which indicates that there are compelling features available to support DIY investors.

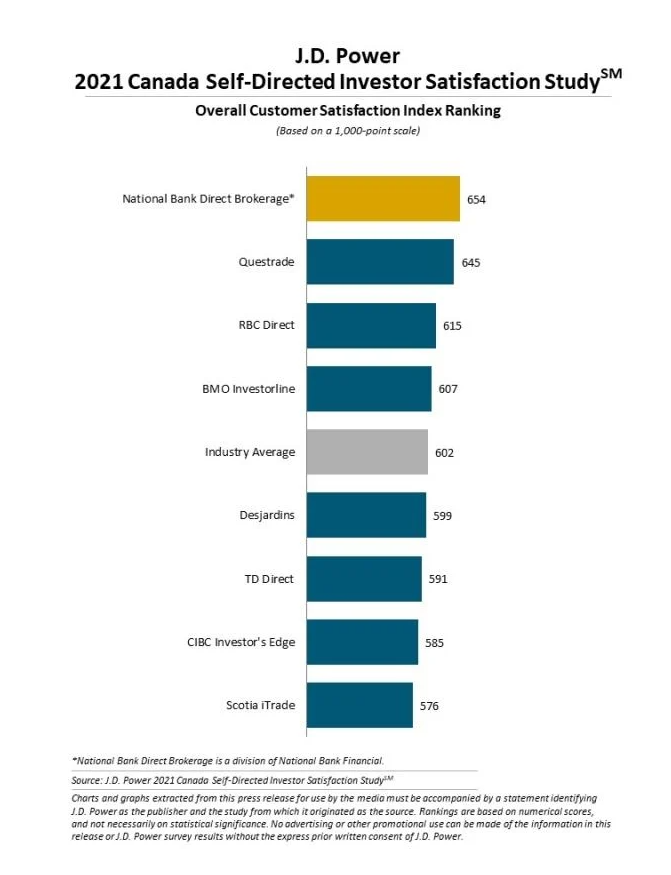

Finally, J.D. Power’s Self-Directed Investor Satisfaction Study, which measures the “voice of customer” perspective, found that Scotia iTRADE ranked last among Canadian online brokerages in terms of satisfaction, scoring 576 out of a possible 1,000 point scale.

In response to the service shortfall pointed out by Mr. Wells, Scotia’s official position appears to define the issue, in part, as a resource constraint at the contact centre level, an indirect admission that “wait times” are likely a driver of dissatisfaction with the service experience.

Of course, without providing specifics as to the headcount providing support and how many customers it is providing support to, it is difficult to know how big of a difference, in absolute terms, 32% more resources translates into. Earlier this month, for example, users of the iTRADE platform reported having to wait hours to contact customer service at iTRADE over a technical glitch. In contrast, at least one peer firm, BMO InvestorLine, has been exceptionally transparent about reporting wait times, which now are reported in minutes (or even seconds). Clearly, for Scotia iTRADE there’s a lot more work to be done with call centre wait times to get them to a competitive level.

Not able to access itrade for 4 hours. Called the call center 3 hrs wait time amd still waiting. Worse bank and it happened before. They dont care when u call. They say its the way it is and we are sorry. Scotia lost a customer here for life.

If there is one point that jumps out about Mr. Wells’ specific question, it is related to the investment products and services being discussed. Specifically, options trading and margin lending. Both of these are hallmarks of active and/or sophisticated investors – precisely the kind of online investor that almost every online brokerage considers to be of the highest value.

As such, it is particularly damaging that a client with this profile is coming forward with this kind of service experience. It is a fair assumption that Mr. Wells is not alone, and as such, shareholders and potentially high value clients may view these comments as a red flag.

What we did learn from the response to Mr. Wells’ question, however, is that Scotia iTRADE is planning to launch a new mobile app this summer, as well as another active trading platform coming later this year. A quick look at the Scotia iTRADE mobile app rankings for the iPhone (1.3 stars out of 5) and for the iTRADE Android app (1.4 stars out of 5) show that a new mobile app experience is long overdue and the expectations for things to improve substantially are high. No pressure.

The reality for Scotia iTRADE is that despite new technology being a welcomed change, launching a new online trading platform (let alone two) will be a big lift requiring solid execution from multiple teams. Based on the roll outs from other online brokerages of new platforms, it will likely take time and lots (and lots) of communication with clients to avoid a flood of calls to the customer service channel and confusion that typically accompanies a major update. And whenever there is confusion or delay, the most active investors – aka some of the most sophisticated ones – are the loudest to speak up about things going wrong. Again, no pressure.

Retention Please

Finally, another revealing data point relates to client growth (aka turnover or “churn”).

As a shareholder, part of Mr. Wells’ concerns focused on customer attrition. Rightly so, because Scotiabank, like any other business, requires either more revenue per customer or more customers to grow. Ms. Griffiths pointed out in her response, however, that numbers on client turnover are reviewed monthly and that Scotia iTRADE continues to attract more clients than it is losing.

Without the benefit of specific numbers, it is hard to quantify that increase, and, importantly, over what time frame. Regular readers of the Roundup know that we track customer growth (or contraction) trends at US online brokerages fairly closely. Unlike the publicly traded US online brokerages, Canadian online brokerages do not report this information in any regulatory filing, so while some online brokerages cite strength in account openings or the number of clients, there is no objective way to validate that information nor is there associated information that goes along with that data. Specifically, there is no data associated with the number of clients that would indicate the value of those clients either in terms of average assets or trading activity – metrics that as a shareholder would directly enable to gauge if Scotia iTRADE is attracting (and retaining) the right mix of clients.

Uncomfortable Questions

The paradox of Scotia iTRADE is that despite having a strong feature set and value proposition (now) for self-directed investors, there is little in the way of regular awareness campaigns or creative approaches to engage with self-directed investors to let them know about these features.

Scotia iTRADE now has over 100 commission-free ETFs (up from 49 last year), strong ranking scores from Surviscor, and average scores from Globe and Mail, as well as a powerful set of research and insight tools.

That said, without telegraphing what they’re working on to a broader audience or keeping pace with what peer firms such as BMO InvestorLine, RBC Direct Investing and TD Direct Investing are clearly working towards in content development – let alone firms like National Bank Direct Brokerage in pricing – it appears that not only are Mr. Wells’ concerns well founded, but they will also continue to lead to more uncomfortable questions.

Now that Scotia iTRADE doesn’t have a channel of its own to steer that discussion, it only leaves shareholders, clients,m and other DIY investors who still know about this online brokerage to wonder aloud what happened to Scotia iTRADE?

Where did scotia iTRADE twitter go?

— Canadian Jennifer 🇨🇦 (@cdntradegrljenn) April 13, 2022

Spring is in the Airwaves

Spring is the season of change and that is exactly the theme of an upcoming webinar where yours truly will be appearing on a panel discussion opening an online trading account.

The Spring into ETF Investing series, presented by BMO Exchange Traded Funds as part of their ETF Market Insights, will be broadcast on April 29 and May 6 and will feature guests from the world of capital markets and personal finance discussing a variety of topics related to ETFs and wealth management.

Tune in on April 29 (or catch the replay on YouTube) for two episodes, one episode on generating monthly income using ETFs and the second on opening an online trading account. Viewers can either register for the webinar in advance or watch the session live on YouTube.

From the Forums

Ready for Change

If you thought we’re the only ones talking about Scotia iTRADE, guess again. In this post on reddit, one very frustrated Scotia iTRADE user asks for more information on when changes will be coming to their platform.

Flow of Funds

Yet another post about Scotia iTRADE, but this time some good news. This helpful redditor posted links to new commission-free ETFs offered by Scotia iTRADE. The new list of ETFs that are commission basically doubles the number previously available, with just over 100 ETFs now available to trade commission-free.

Into the Close

What a wild ride it’s been. The combination of a short week but no shortage of stock market activities courtesy of earnings means that even more fun was packed into fewer days. Between Elon Musk on Twitter and budget buzz still going strong, Easter eggs are still rolling in.

Change is certainly life’s only constant. And even though, historically, change has been relatively slow to take effect among Canadian online brokerages, when it does show up, the effects tend to endure. As we steer into the season of change, it seems like both the pace and breadth of change are starting to accelerate, with some remarkable developments.

In this (we’ll call it “toddler time-distorted”) edition of the Roundup, we look at an unusual pattern emerging in the deals and promotions activity at Canadian online brokerages and what it could signal for promotions going forward. Next, we highlight a new look that one online brokerage is sporting for spring, and whether it is dressed in what the cool kids are into these days. Finally, we’ll wrap up with some timely topics self-directed investors are chatting about online.

Usually around the start of each month we go through the latest deals and promotions to see what new offers have shown up and whether there are any interesting developments in the ongoing race to garner attention (and assets) from self-directed investors. This month, however, there was a signal of continued unusual activity among the Canadian online brokers that suggests there are some interesting changes coming to the way in which online brokerages create and launch promotions.

Of course, “change” is a relative term, so, before diving into what seems to be evolving with online brokerage deals and promotions, it’s useful to get a sense of what is “typical.”

Although many online investors now know that Canadian online brokerages offer deals and promotions, especially during RRSP season, that hasn’t always been the case. There was a time many years ago that most Canadian online brokerages were reluctant to use promotions and incentives to attract in new self-directed investors. Interestingly, as commission prices began to drop in a meaningful way, roughly around 2014, so too, it seemed did the resistance to trying out using offers to encourage new users to try out a brokerage.

At that time, one of the most active Canadian online brokerages when it came to special offers or promotions was Questrade – who aside from much lower commission prices than their peers – was a constant name to watch because they ran so many promotional offers. The kinds of promotions they ran ranged from various commission-free trade offers to promotions featuring a free iPad.

It was not long after other online brokerages lowered their commission prices, that one of the first big shifts in the deals and promotions activity took place: Questrade stopped offering so many promotions.

Instead of offering so many different promotions, Questrade decided to consolidate their offers and focus their promotional offers on their affiliate program and referral bonuses (and later launching TV ads). Many of the same promotions, such as their five free trades or first month free, are still available today. Regardless of the season – including RRSP season – Questrade’s strategy was still the same when it came to promotions. Namely, stick to their core offers.

It’s difficult to characterize just how significant of a shift that was at the time; however, by the time Questrade did ramp down, other online brokerages, notably BMO InvestorLine, had picked up the practice of regular promotions outside of RRSP season. In fact, since that time, BMO InvestorLine has effectively carried the torch for launching “new promotions” just about every season.

So, if there was one online brokerage in Canada that we did not expect to see a break in promotional cadence, it was BMO InvestorLine. And yet, this month that is exactly what’s taken place.

To be fair, BMO InvestorLine hitting pause on deals is not without precedent. That said, the last time they did so was near the start of the pandemic, when BMO InvestorLine’s unprecedented investor interest overwhelmed systems.

This time, however, there isn’t a rush of investors flooding the systems of BMO InvestorLine with new applicants, which begs the question, what would cause BMO InvestorLine to pause offering an already live tiered cash back promotion at a time when major rivals still have open offers?

It’s difficult to know exactly why, however, it seems that shuttering an active deal is likely the result of something abrupt instead of something planned, especially given the timing being so close to the launch of their latest cash back promotion.

Perhaps the economics of a tiered cash back offer simply don’t work for BMO InvestorLine, or perhaps the costs of running a campaign to acquire new clients exceeded the benefit those clients would bring. The latter point is one of the drivers behind online brokerages typically choosing to launch promotions during RRSP season instead of during the whole year. When online investors are “in market” for a new online brokerage or seeking to park new assets in an account, as is the case during RRSP season, online brokerages want to be as visible as possible.

That said, instead of stopping promotions outside of RRSP season, one of the strategies BMO InvestorLine has employed in the past was to raise the deposit threshold at which an individual investor could qualify for a promotion. Thus, instead of requiring a minimum deposit of $15,000, BMO InvestorLine could raise the minimum deposit to $50,000 so that only those individuals who bring the kind of value BMO is seeking qualify for incentives.

So, though speculative, if costs of a program suddenly get put under the microscope to the point that they lead to a decision to cut loose a promotion in midstream, then a good candidate reason why would be a “cost cutting” program. And for that to take place at BMO InvestorLine, a bank-owned brokerage, that is very interesting timing indeed. If, after all of the years of running this program, something fundamentally has changed (or is about to) for promotions-led acquisition, it does beg the question as to what BMO is encountering now that makes the math for promotions untenable at this time.

Though the online promotion of the deal is now gone, self-directed investors interested in the cash back promotion at BMO InvestorLine may be able to access the offer via customer service touch points (e.g. in branch) on a case by case basis. When a client is of sufficiently high value (what that value is, we don’t yet know), then they might be offered a cash back incentive.

The latest move by BMO InvestorLine to shutter an active offer is a step change for an online brokerage that has almost consistently leaned into “always on” promotions and bears a resemblance to the structural shift in promotional strategy that Questrade undertook many years ago. Unlike that decision, however, BMO InvestorLine does not have the same magnitude of affiliate channels nor social media community support that Questrade had when it decided to shift its promotions strategy.

Instead of being a leader among Canadian bank-owned online brokerages when it comes to promotional activity, it seems BMO InvestorLine is more content to run with the pack. With no other big bank-owned online brokerages currently offering cash back promotions right now, all attention for self-directed investors looking for a cash back deal on a new trading account is being directed to Qtrade Direct Investing.

The bigger consequence to bowing out of the post RRSP season promotions race may not be felt for some time but will almost certainly resurface again next RRSP season. One of the biggest benefits of an always on campaign is to continuously attract attention of investors and to be among the list of names those investors consider when the need for a solution arises. In this case, BMO stepping back simply opens the door to another lesser known or not historically active name to fill that void.

An alternate view is that online brokers may also be more willing to be agile when it comes to promotional activity. A case in point is the current cash back promotion from Qtrade Direct Investing.

Qtrade did something highly unusual at the beginning of this year by revising upward the amount they were willing to offer to new clients. They did not “set it and forget it” with the deal that launched last year but rather saw that their offer was not nearly as competitive as their peers and adjusted accordingly.

The fact that BMO InvestorLine was the only big bank-owned online brokerage in market with a cash back promotion perhaps made them realize they were overspending to acquire new clients. That they were willing to do so mid-campaign is maybe a sign of different kind of structural change: online brokerages are becoming nimbler.

This year alone we’ve seen Qtrade Direct Investing change deal amounts, BMO InvestorLine effectively shut down an already live deal, and RBC Direct Investing move around the expiry date on an unprecedented commission-free trade offer. If there was ever a case for expecting the unexpected, Canadian online brokerages seem to have made it their theme for 2022.

CI Direct Trading Sporting a New Look

Spring seems like the opportune moment for new beginnings. This month, CI Direct Trading, the brand formerly known as Virtual Brokers, officially rolled out their new public-facing website. Gone is the familiar combination of red, black and white, and instead, the new website reflects the last stage in the integration of Virtual Brokers with the CI Financial common look and feel.

While a “new” website isn’t necessarily a big step change, building a new online brokerage website in an ultra-competitive environment does present an opportunity to intentionally lean into the brand identity. Secondarily, for seasoned observers, it offers a glimpse into where the priorities are for a particular provider.

In the case of the new CI Direct Trading website, there are a number of interesting observations to comment on; however, the biggest theme that jumps out is integration.

Unlike Virtual Brokers, which was effectively a standalone online brokerage, CI Direct Trading’s new site was intended to fold the online brokerage into the CI Financial ecosystem. And, at first blush, it appears they’ve done so – perhaps too well.

In fact, in the drive to create a common look and feel between brands, the point at which CI Direct Trading starts and where CI Direct Investing stops is very blurry.

Navigating between the CI Direct Investing and CI Direct Trading is so seamless that as a user, you wouldn’t know where you are unless you look at the logo on the page, and even then, you’d have to really pay attention to the small text under the word “direct” in the logo. Recall that one of the principles of user-centred design is to answer a simple question: am I in the right place? On the new CI Direct Trading website, the answer for DIY investors in particular is unclear.

On a more nuanced note, the decision to use the names “CI Direct Investing” and “CI Direct Trading” is confusing because almost no other online brokerage in Canada uses the term “Direct Trading” in their names. Three big names in the “Direct Investing” space jump out, for example:

Qtrade Direct Investing

RBC Direct Investing

TD Direct Investing

Virtual Brokers used to be a direct competitor to these particular providers; however, CI Direct Investing (rather than Direct Trading) seems like it would be the place where a user would look to find a service similar to Qtrade Direct Investing, TD Direct Investing or RBC Direct Investing. Except, they would be incorrect. CI Direct Investing is more akin to a roboadvisor solution, not a DIY one.

Although it seems like semantics, in reality, the “DIY investor” industry has been undergoing its own identity crisis for the past decade. Ten years ago, the entire space was almost uniformly calling themselves “discount brokerages,” then it shifted to “online brokerages,” and now they are positioning themselves as “direct investing” solutions providers.

Why this matters so much is because when it comes to being found online, something that is exceptionally important in a hypercompetitive environment, individual investors are going to search based on what they know and think is the term they need to use in order to access the category of service providers. When the category shifts, so too does the audience searching for it.

Another interesting theme is that the new website leans heavily into the “less is more” look. There are fewer options and less text as well as clear headings so that there is less information to have to parse through on the front page. From a visual perspective, there is also a heavy presence of mobile screens, a decision that undoubtedly is intended to relate to a generation of “mobile first” traders.

In a tinge of irony, the screenshots of the CI Direct Trading iPhone app show the symbol of a well-known Canadian bank (TD) instead of using the opportunity to have the publicly-traded CI Financial ticker (CIX) on there.

Even in the app store, the Virtual Brokers legacy association is still visible too, a reminder that all brand touch points need to be considered in the rebrand process. Of greater consequence, however, is that the legacy star ratings for the app experience are likely to impact user impressions on the brand. With a 2.5 star rating on the Apple App Store for CI Direct Trading, there is much work to be done to improve the perception of the mobile app as being an enjoyable way to engage with the service, especially with the mobile-first crowd.

When Virtual Brokers was acquired by CI Financial in 2017, it was unclear what direction the popular online brokerage would go in. Fast forward to today, it is now clearer that the successor to VB, CI Direct Trading is offering many of the same features and pricing as Virtual Brokers but is wrapping itself into the CI Financial ecosystem.

It has been a relatively quiet four years since the integration was first announced but now it seems the real work will begin for CI Direct Trading to be able to tell its story to online investors (traders?) and establish its niche in a very crowded field.

If the new design is a signal they’re looking to court a younger generation of investors, simplifying the website is a step in the right direction. Clearly, though, there is much work to be done in the seasons ahead to evoke the same kind of emotion, curiosity, and enthusiasm that their direct competitors have already managed to successfully achieve.

From the Forums

Transferrable Skills

Moving day is always a chore. When it comes to moving mutual funds, however, it’s a problem that needs more than pizza to solve. One reddit user reaches out to the community of investors in this post for some guidance on how to navigate transferring away from Manulife and into a popular online broker.

Under the Influencer

A big theme among online brokerages heading into this year has been investor education. An interesting discussion emerged in this reddit post about seeking out “education” on investing and trading from a relatively well-known Canadian personal finance influencer.

Into the Close

That’s a wrap on another edition of the Roundup. If news among the online brokerage space is anything like the weather in April, it’s going to be a mixed bag of activity throughout the month. For the loyal readers that have managed to make it this far, we’re also going to be sharing more updates in the weeks ahead on the new special SparxTrading Pro and other tools we’ve been working on, so be sure to tune in for sunnier news coming around the corner. Until then, keep your powder and yourselves dry, you never know what might come up as an interesting buy.

Seasoned traders understand that in volatile situations, sometimes it’s best to sit on your hands. Though that advice would certainly be applicable outside the world of self-directed investing (*cough* Will Smith *cough*), within the world of self-directed investing, activity is tied to profitability, at least for online brokerages. So, it is a fine balance between taking action and being patient.

In this late-in-the-week edition of the Roundup, we check in on an important shift taking place at Canadian online brokerages that will see mutual funds come back into the spotlight for the next several months. Speaking of near term visibility, our next story looks at what one popular US online brokerage is noticing with respect to skepticism on the part of active investors. To close out, we highlight investor chatter about mutual fund commission charges and margin rate questions.

Can’t Fight this Fee-ing Anymore

One of the core tenets of self-directed investing is controlling or minimizing unnecessary costs.

Despite the characterization or popular mythology around self-directed investing as a “fast money” or a high activity endeavour, a significant portion of online investors are not very active and prefer to “take it slow and steady.” For example, a study on retail investors conducted by the Ontario Securities Commission in 2021 found that 43% of investors surveyed make fewer than 10 trades per year and 31% make 11 to 50 trades per year.

While activity is certainly influenced by what is out there to buy, prevailing opinions also suggest that up-front commissions have a part to play in influencing purchase behaviour. The rise and popularity of the zero-commission trading online brokerage Robinhood provided a dramatic example of this in the US, as has the growth of Wealthsimple Trade in Canada.

As most of us have come to learn, though, there is no such thing as a free lunch.

Despite the reluctance to go to zero commission trading on stocks, Canadian online brokerages are not unfamiliar with the practice of zero commission trading on mutual funds. Unfortunately, for many Canadian online investors, this has resulted in a scenario in which self-directed investors have been paying commissions for things that technically they’re not supposed to be paying commissions for from an online brokerage, namely, advice.

Though this story has taken a backseat during the pandemic, the timing of the deadline for online brokerages to transition investors into suitable alternative investments is nearing. As such, the response by some online brokerages to start charging commissions on mutual fund trades is surfacing in the news as is the access to previously unavailable mutual funds.

This month, for example, CIBC Investor’s Edge started to charge their standard commission rate, $6.95, to buy or sell mutual fund units. RBC Direct Investing rolled out new pricing this month as well, charging 1% of the gross trade amount up to a maximum of $50 for purchases of mutual funds. On the other end of the spectrum, it’s business as usual with no charge for mutual fund purchases at TD Direct Investing and BMO InvestorLine.

A side benefit of the new regulatory requirements is expanded choice for some online investors at firms like RBC Direct Investing. Previously, and much to the chagrin of self-directed investors, Mawer mutual funds were not available at RBC Direct Investing. As of this month, however, Mawer Investment Management announced that 13 of their funds are available at RBC Direct Investing.

With new regulations governing trailing commissions set to take effect June 1, there are still pockets of uncertainty relating to charges for mutual fund trades. The structural shift in product lines has been taking place over the past two years against the backdrop of the pandemic. However, with a deadline looming, the flurry of activity and announcements from online brokerages early this year suggests they are cutting it a bit close as far as communicating these changes to their clients. Ultimately, that could prompt a customer service risk, especially if there are any big market shocks that set off a surge of requests for contact centre support.

Although fundamentally different in spirit and appeal than individual equities or ETFs, the fact that mutual funds remain a very popular choice for certain DIY investors who do business with bank-owned online brokerages (say, those who might remember or know that REO Speedwagon hit referenced in this section’s title?) means that how individual banks approach the selection and pricing of mutual funds can be a differentiating factor. That is especially important to consider as online brokerages attempt to provision for an influx of younger investors.

We want people to come for the advice and stay for the performance. So, younger individuals who don’t want to take advice and want to go DIY on their own. Generally speaking, those don’t work out that well, right? That said, we also know that we have sophisticated investors who do want to run their own money as part of managing their overall portfolio, so they may have a relationship with a portfolio manager and run 15% on their own, in our case in an iTRADE account. And we want to support both of those positions.

And I think what you’re going to continue to see, I think, is us introducing more channel options to address the different needs of each of those segments. I would say as a fiduciary, and we are very clear about this with the regulators, we are nervous about the propagation of — you can build your own portfolio and retire 15 years earlier by saving a few dollars on fees. We think it’s a very dangerous message to send to Canadians at a time where they’re very anxious even about their mortgage debt. People should remember, it’s very important for Canadians to get advice on banking, investments, insurance and debt, not just investments. And I think as we begin to see more and more feedback from young Canadians about how are they going to save for a mortgage, save for a house, they have to come in for a conversation on that. They can’t do that on their own around the kitchen table. Historically speaking, it’s not successful.

Another interesting angle to the mutual fund shuffle taking place at online brokerages is that it offers a hint of how commission free trading could be handled at bank-owned online brokerages. A great case in point is TD Easy Trade. The new service allows for 50 commission-free trades of stocks but has limited selection of ETFs to just TD products.

Like “commission free” mutual funds, commission free trading at bank-owned online brokerages is going to have to come with some kind of value capture.

Stepping Aside: Interactive Brokers’ Clients Prefer to Wait and See

One of the strategic places to pay attention to in the online brokerage market is with active investors. In a world of commission-free trading, it is interesting to ask who would actually pay commissions to an online brokerage for trading services. The answer: Interactive Brokers clients would.

In a short interview on CNBC, founder of Interactive Brokers, Thomas Peterffy, shared some interesting details about the status of cash and margin position for Interactive Brokers’ clients that seemed to suggest that they are atypically not borrowing money nor putting cash into positions. Of note, the typical profile of a customer is also something Peterffy shared, since the profile of assets Interactive Brokers customers has is significantly larger than say, Robinhood customers.

Why this was of particular interest is that, typically, volatile markets are favoured by active traders.

Ahead of periods of heightened uncertainty, Interactive Brokers has served as an interesting harbinger of near-term behaviour. They are typically agile at tightening margin requirements if they foresee risk to their firm. In this case, the conclusion arrived at by Peterffy is that Interactive Brokers clients aren’t buying in this market because they don’t buy the strength of the rally. They are selling, it seems, into strength.

If interest rates rising are a disincentive for margin trading, however, it would suggest that there is limited upside, at least in the near to medium term. The fact that investors that are both knowledgeable about markets and who are prepared to pay for quality trade execution are not seeing a favourable risk/reward seems to paint a cautionary tale at least to that style of investing activity.

The consequence of activity pulling back for stock trading among the most valuable category of online brokerage clients is something that would be difficult to approximate the impact to among Canadian online brokerages; however, it almost goes without saying that it isn’t ideal.

This active group is likely to play a much more prominent role in the planning for online brokerages going forward since they not only typically trade stocks but also options. And, as data has shown, the small category of very active traders (50+ trades per month) can generate substantial revenue (and are prepared to do so) so long as the trading experience is reliable.

Getting those investors to pay attention to online brokerages against a backdrop where there is skepticism on market direction and rising interest rates will be especially challenging. The limited number of Canadian online brokerages that could cater to these active traders appear to have their work cut out for them.

From the Forums

Take a Hike

The headline news is replete with interest rate chatter. Interesting (no pun intended) then that the pace of those rate changes is also in the spotlight and why one eagle-eyed investor in this post noted a rather sharp increase in the margin rates at a popular bank-owned brokerage.

Fund Times

Chatter around mutual funds at online brokerages is at an unusual high point. Commissions are once again in the spotlight and one question from a Reddit user is certainly indicative of what others are thinking: which online brokerages are now directly charging (or not) for mutual fund purchases and sales.

Into the Close

That’s a wrap on another edition of the Roundup. It’s been a choppy past few days; however, all eyes continue to be fixed on how fast and furious interest rates are going to climb. Whether we can all make the leap to a new normal of interest rates is what everyone is working to figure out.

With Tom Brady seemingly defying the laws of aging by announcing his take back on retiring, it goes to show that age is truly just a number. It’s a fitting theme, especially at online brokerages in Canada and the US, as firms in this space are only just beginning to wrap their heads around the surge in young investors who’ve embraced self-directed investing.

In this edition of the Roundup, we attempt to wade into multiple pools of data about young investors entering into the world of self-directed investing and the impact this group is having on online brokerages in Canada and the US. We cap things off with a quick scan of post-RRSP season commentary from the investor forums.

Young Investors Making Waves

One of the interesting things about tsunamis is that when they first begin, they don’t appear to be very big at all. Over distance and time, however, their size and force are undeniable.

Although not a new story by any means, the “rise of the retail investor” is one whose effects are now gathering in intensity, and impacts are becoming increasingly more visible across the self-directed investing landscape, in particular, at online brokerages.

Tracking this wave has not been easy, especially in Canada, but a slate of recent publications and feature launches from Canadian online brokerages, combined with data and developments from US online brokerages, paint a picture of an industry that is quickly trying to understand and cater to this new generation of investors.

A Sea of Change

Earlier this year, TD made a splash of its own by launching TD Easy Trade, the successor to GoalAssist. There are certainly many interesting things to comment on here; however, at the top of the list of features that got many people talking was the 50 commission-free trades per year that come standard with the platform.

At first blush, it certainly seems like this “mobile-first” trading experience was engineered to supplant Wealthsimple Trade; however, the reality is more nuanced. Yes, Easy Trade and Wealthsimple Trade (even from a branding perspective) are comparable in design and features, but the launch of Easy Trade this year is less likely the result of Wealthsimple Trade per se and more likely because of the seismic shift in self-directed investor demographics during the pandemic. After all, TD Direct Investing is widely cited as having the largest market share in Canada of online brokerage accounts, and as popular as Wealthsimple Trade has become, it is still likely far behind other online brokerages either in terms of number of clients or assets under management, or both. As such, Wealthsimple Trade, now a competitor to be considered was not really a “threat.”

The press release of the TD Easy Trade launch was, perhaps, the most telling. Specifically, the quote by Tony Ierullo, TD Direct Investing’s Vice President, New to Investing and Emerging Investor Solutions. Ierullo stated:

“During the pandemic, we saw a significant increase in demand for online investing, with more people trying DIY investing from home, and for the first time. As a result, trades and new account openings hit record highs. This growth in new accounts and trading volumes was driven largely by new and younger investors, which is why it was important to us to launch an app that is easy-to-use, with low trading fees and available support to ensure investing is accessible to this emerging, fast growing investing segment.”

Rather than competition driving the change, it was customers. And lots of them.

Though TD’s release was short on specifics about this group of new investors, another bank-owned online brokerage, RBC Direct Investing, published the results of a survey they commissioned (no pun intended) to understand young investors.

RBC Direct Investing’s President & CEO, Lori Darlington, sat down with Sparx Trading to dive into the data on new self-directed investors (check out the full interview with Lori Darlington) and it was fascinating to see the extent to which younger investors are now shaping the conversation and direction of established online brokerages. As telegraphed in the latest edition of the Look Back / Look Ahead series, RBC Direct Investing had experienced a significant influx of younger investors during the pandemic.

Their latest survey, however, revealed a more precise figure: nearly half of new clients at RBC Direct Investing that joined during the pandemic were under the age of 35.

Although RBC Direct Investing was the one who published a more concrete number, the reality is that these results are likely typical at most Canadian online brokerages. And, in many ways, this survey offers some very compelling takeaways for all Canadian online brokerages, as well as those watching the industry closely.

One interesting nuance of the data, however, shows just how important the sampling frame – or when the sample was collected – is to the conclusions to be derived from surveys.

In April 2021, just after the meme-stock mania hit a crescendo, the Ontario Securities Commission (OSC) published their survey of self-directed investors in Canada. Though timely, the survey of 2,000 Canadian investors was fielded between November 17 and December 6, 2020. In that survey, only 19% of respondents indicated that they had an account opened for a year or less. In contrast, in the RBC Direct Investing poll, 1,530 investors were surveyed between October 26 and November 5, 2021, with 900 of those being DIY investors and 630 “interested in” DIY investing. The figures from the latest RBC Direct Investing research point to a much higher proportion of new investors stepping into the markets in 2021 than was the case in 2020.

To help compete the picture though, another bank-owned online brokerage, BMO InvestorLine, shared numerical data on the numbers of new account in the Canadian online brokerage segment all the way back to 2014. Although the source of the data should be treated with a grain of salt (i.e. unlike data that comes from publicly traded online brokerages in the US, the Canadian data is based on voluntary disclosure, and thus cannot be independently verified), the picture does line up with data from online brokerages in the US. New online brokerage accounts surged to unprecedented levels in early 2021.

Why this matters so much is because when new investors step into a market largely forms a crucial first impression of what constitutes normal.

For an overwhelming majority of new investors, in particular young investors, volatility and opportunity for once-in-a-generation (maybe?) price disruptions were a catalyst to opening new trading accounts and trading stocks online. Meanwhile, older and seasoned investors saw volatility as a reason to seek out safety (or sensibly “do nothing”). And therein lies a crucial difference between the new cohort of investors compared to established investors. New investors are clearly willing to trade – even under circumstances where risk (i.e. volatility) is extreme. And their entry into the world of self-directed investing happened against the contextual backdrop of enormous global disruption and economic distortion.

The places and people that new investors turned to for direction during the pandemic, as well as what they invested in and how they invest, were all very different for younger investors who stepped into the market in the past 18 months compared to the previous almost 18 years.

How Can Online Brokerages Ride the Wave?

There’s lots more than can (and will be) said about the rising influence of younger investors among Canadian online brokerages. Thematically, however, it is immediately clear that focusing on “price and device” underpins the first leg of a strategy for online brokerages.

In the device category, as recently as this past week, Interactive Brokers announced the launch of their new trading app IBKR GlobalTrader, a simplified version of their trading experience tailored specifically towards newer investors. It happens to be a mobile app, with fewer features (i.e. less complexity) than the typical Trader Workstation, and thus is expected to be easier to use.

The fact that bank-owned online brokerages as well as active-trader-focused brokerages are looking at gaining market share of the same segment of users is indicative of the importance of winning market share with newer investors.

In the price category, in addition to lower standard commission prices, making the process of regular investing behaviour frictionless would be appealing.

Features like fractional shares or commission-free ETFs (like the ones that people want, not just the ones that brokerages are willing to make available) have curb appeal for newer investors. It’s no accident that Amazon decided to split their stock recently which then made the stock seemingly more accessible to stock and options traders.

Other than prices and devices, however, Canadian online brokerages appear to be leaning hard into investor-oriented content. From magazines to videos to podcasts, there is a growing ecosystem of content that online brokerages are making available to self-directed investors that is partly educational and partly contextual. With so much information about investing available online, however, it will be a challenge for online brokerages to balance providing a “streamlined” user experience and a wealth of content around investing topics.

Conclusion

New investors are reshaping the online brokerage industry the world over. For many online brokerages, navigating this new normal is a serious exercise in rapid adaptation.

The sudden surge in self-directed investors overwhelmed existing systems because those systems were designed around “traditional” thinking, and the past two years have shown that, going forward, online brokerages need to rethink what investing online could look like.

As the wave of change continues to evolve, one of the biggest challenges to face online brokerages won’t be getting new online investors to pay attention, it will be to keep it.

From the Forums

Fee-ling’s Not Mutual

Although there is a lot of conversation among self-directed investors about ETFs and stocks, mutual funds are still a very popular vehicle used by Canadians to build wealth. In this post from Reddit, however, one investor is re-thinking using mutual funds because of a recent fee change at one big bank-owned online broker.

Savvy vs Saasy

Subscriptions are all the rage, especially with tech companies. But will paying a monthly fee for services pan out for self-directed investors? One Canadian online brokerage seems to think so as they explore a monthly fee for more premium features. Investors in this post on Reddit, however, beg to differ.

Into the Close

That’s a wrap on another in-the-middle-of-the-week edition of the Roundup. Perhaps the only upside to Daylight Savings is that St. Patrick’s Day shows up an hour earlier. Here’s to channeling lots of green in stock charts and tree branches, as well as a cheers to new beginnings and signs of spring. We definitely need all of it.

Let’s call a spade a spade: things are in a terrible state. While we continue to watch from afar and hope that peace comes quickly to Ukraine, markets and investors closer to home are trying to digest world events having local consequences. And right now, we could all use something uplifting.

Fortunately, there are a few bright spots in this edition of the Weekly Roundup. To begin, we review the latest online brokerage deals and promotions, with a detailed look at how developments during the RRSP season portend what DIY investors can expect through the rest of the year. From there, we dive into a master class in continued growth by Interactive Brokers, whose latest metrics reveal that they’ve successfully navigated the new normal. Finally, tune into chatter from the investor forums to see what self-directed investors were focused on (other than oil prices).

Deals and Promotions: Rise of the Hybrids

While the holiday season is typically the time of year for gifts, it seems this year it was the RRSP season that gave self-directed investors the gift that keeps on giving: online brokerage deal extensions.

Things around the Canadian online brokerage industry are a bit unusual these days (see next story for more). Prior to the pandemic, there was a trend of online brokerages offering incentives and promotions that would typically start in November and last until the RRSP contribution deadline at the beginning of March the following year.

While last year was characterized by a tsunami of new investors clamoring to open online brokerage accounts, this year traffic is comparably quieter and thankfully more measured. And, despite crowd sizes returning to more manageable levels for online brokerages, the deals and promotions offered around RRSP season reflect a massive step change in the promotional landscape, driven in large part by increased competition and a whole new set of investors that are looking at trading online.

Before diving into the analysis of March’s deals and promotions reveal about the current competitive landscape, let’s begin with a recap of who’s in and who’s out.

A tale of two offers

The biggest promotions that expired at the beginning of March were from TD Direct Investing and CIBC Investor’s Edge. Both bank-owned brokerages, both cash back promotions.

What is interesting, however, is that on a year-over-year basis, the profile of the offer from CIBC Investor’s Edge was about the same, whereas for TD Direct Investing the minimum deposit requirement dropped 90%, from $15,000 to $1,500. Across multiple deposit tiers, TD Direct Investing also offered the highest (or was tied for highest) cash back amounts.

As small as this sample size is, it is illustrative of how Canadian online brokerages appeared to approach RRSP season this year.

On the one hand, there are firms that chose to stick to the traditional script, and on the other, firms that took a dramatically different route. Based on the numbers, it is clear that TD Direct Investing employed a different playbook, whereas CIBC Investor’s Edge stuck to their familiar game plan.

Perhaps it was the aggressive promotional approach of TD Direct Investing as well as the presence in the background of zero-commission trading at National Bank Direct Brokerage, Desjardins Online Brokerage, and Wealthsimple Trade that raised the stakes for online brokerage promotions during RRSP season.

That said, as the RRSP season went on, we witnessed three exceptional developments that suggest the current competitive landscape among Canadian online brokerages has shifted in a direction we believe is bullish for self-directed investors looking for a promotion when opening an online trading account.

A series of fortunate events

The first big shift in tactic came from Qtrade Direct Investing. At the outset of the RRSP season, Qtrade launched a cash back offer that looked like past offers. That is, they weren’t trying to be “first” when it came to cash back amounts.

That all changed in late January when Qtrade Direct Investing revised their cash back offering upwards and lowered the threshold to qualify for the promotions as well. They lowered their minimum deposit requirement from $15,000 to $5,000 and raised their minimum deposit bonus from $50 to $100. On a year over year basis, the revised Qtrade promotion was 80% lower for the minimum deposit threshold (from $25,000 down to $5,000) and two times higher in terms of minimum bonus. And it didn’t stop there.

Qtrade Direct Investing also raised their cash back amounts across numerous deposit tiers, matching the top bonus amounts in almost all of them. The only range where Qtrade Direct Investing was not tied for the highest cash back amount was in the $25,000 to $50,000 tier.

And this brings us to the second big development during the RRSP season, which is promotion extensions.

Historically, the expiry date of most online brokerage promotions would coincide with the end of the RRSP contribution season. This year, however, we saw expiry dates stretch out well beyond that point into March and April. And, as the RRSP season drew to a close, we started to notice deal extensions further into the calendar year.

For example, Qtrade’s cash back promotion now expires at the end of May (moved from an original expiry at the end of March). The RBC Direct Investing promotion, a fascinating development in its own right because of the number of commission-free trades (100) and term over which they can be used (two years), was originally scheduled to expire at the end of April and is now set to expire at the end of October. Joining this list of extensions is BMO InvestorLine, which has now extended its RRSP season cash back promotional offer into the end of May. Scotia iTrade has not extended their current offer (yet?), however, that is set to expire at the beginning of April.

Finally, another telling development during RRSP season this year was the launch of Easy Trade by TD. This new trading platform (which is separate from TD Direct Investing) offers 50 commission-free trades per year to its users. There is no doubt that when one of the largest banks in Canada launches a product that promises 50 commission-free trades per year, that self-directed investors (and other online brokerages) are going to pay attention. And, just in case they weren’t paying attention, TD heavily advertised the launch of Easy Trade during the Super Bowl and is continuing to advertise on social media as well.

Collectively, these developments are bullish for self-directed investors looking for better value (on commission pricing) and suggest that deals and promotions are going to fare more strategically into the approaches of online brokerages in the near term. In particular, those online brokerages that don’t want to drop their standard commission prices can, instead, launch a competitive commission-free trading promotion (as was the case with RBC Direct Investing). The events over this RRSP season also may serve as a harbinger of commission-free trading finally gaining widespread adoption in Canada.

Prior to the launch of full zero-commission trading at National Bank Direct Brokerage, this bank-owned brokerage offered 100 commission-free trades which were good for one year. Eventually, that promotion was superseded by the new pricing scheme. But in taking a measured approach towards zero-commission trading, it stands to reason that they could have reviewed the data associated with that promotion to decide about the impact of going to zero.

As TD showed with Easy Trade, zero-commission trading doesn’t necessarily mean full access to the suite of tools and capabilities that their TD Direct Investing online brokerage platform has.

It’s certainly a salient metaphor these days, but the “hybrid” option (aka unbundling) introduced by TD of paying for some trades or features and not for others could be how other online brokerages who currently charge for commissions approach the new world of zero-commission trading.

If other online brokerages follow suit, then just like at the pump, DIY investors looking for premium will be prepared to pay up. For everyone else, however, getting started with investing appears to be getting a lot cheaper.

Interactive Brokers: Numbers Reveal a Winning Formula

As we near the two-year anniversary of the official declaration of a global pandemic by the World Health Organization (March 11, 2020), the true impact of this once in a generation (hopefully) event is starting to become clearer. Although COVID is by no means behind us, almost anyone in the online brokerage industry can attest to how exceptionally different things are now than in the “before times.”

One area that probably doesn’t get much attention, however, is benchmarking. Specifically, how do you compare what’s taken place over the past two years to anything?

As it relates to online brokerages, be they Canadian or US, data from the past two years is showing that the changes to the industry have been profound. In many ways, not only is there a “new normal,” but new approaches are required and many of these are largely going to be written on the fly.

Earlier this month, as per usual, Interactive Brokers released their monthly performance metrics (for February 2022). Contextualizing these numbers, however, is particularly challenging because of how dramatically different the performance figures were in January and February of this year compared to last year. Though it may not be news that 2020 and 2021 were busy times – even by historic standards – what is particularly noteworthy is what you can see when net new account growth is plotted out back to 2019.

Because a picture is worth a thousand words, take a look at this graph of data of net new accounts at Interactive Brokers from 2019 to 2022.

Among the many things that jump out, it is striking to see the step change in interest in trading online that coincides with the start of the pandemic. Even more imposing is the surge in net new accounts in the first three months of 2021. Against that backdrop, the latest account growth figures reported by Interactive Brokers could be good, excellent, or terrible. Thankfully, context matters, and as such even though just under 39 thousand net new accounts represents a month over month decline in February of almost 22%, this still puts the strength of new account growth several times above where things were pre-pandemic.

Surges in interest aside, the longer-term picture points to a sustained interest – at least for Interactive Brokers – in trading online as indicated by net new account opens.

Prior to the pandemic, the average number of net new accounts in a month in 2019 was about 7.6 thousand. Excluding the period between January and March of 2021, the average between March 2020 and February 2022, the average number of net new accounts at Interactive Brokers has climbed to just shy of 38 thousand per month, a whopping 5x increase.

Focusing in on a more recent timeframe, it appears that the launch of cryptocurrency trading at Interactive Brokers in the late summer of last year helped to provide renewed enthusiasm for new account growth. Net new accounts opened in November 2021 (almost 55 thousand) reached the highest level seen since the end of the meme-stock craze in March.

Interactive Brokers’ continued account growth serves as a remarkable example of what is clearly a winning combination for active investors/traders.

Granted, some of the growth in their numbers is from acquisition. However, most new accounts have come through organic growth. Even more fascinating is that a material portion of their new clients have come to Interactive Brokers because of recommendations and referrals from existing clients.

Perhaps most remarkable of all, though, is that this data shows that growth can happen at an online brokerage that has a core business that charges commissions per trade, and against a backdrop where commission-free trading is the norm at many peer firms.

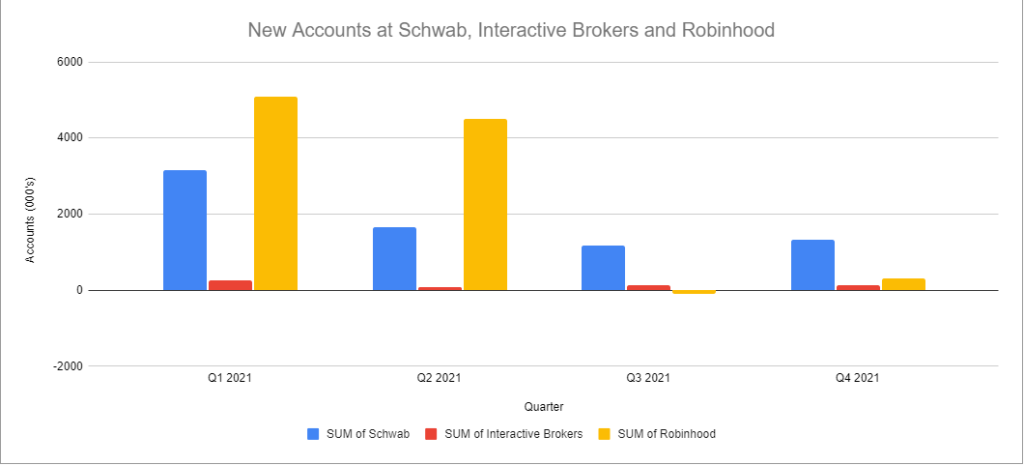

When comparing account growth figures across Interactive Brokers, Schwab, and Robinhood for 2021, it was revealing to see how poorly Robinhood fared against its peer firms in the back half of year – especially in the category of account openings. In contrast, Robinhood, which blew the doors off account growth in early 2021, saw a precipitous drop in account growth once meme-stock momentum faded.

As mentioned above, the truly exceptional nature of what happened in 2021 to the world of online investing makes comparing subsequent time periods against those first few months somewhat futile. The open question for online brokerages is whether the new entrants into the world of online investing are here to stay or simply a temporary phenomenon.

What the longer-term account data provided by Interactive Brokers suggests, however, there is more permanence to new users and continued interest in sophisticated platforms. Robinhood’s latest performance data has shown that especially when it comes to trading stocks, the new cohort of investors and traders were not nearly as interested in that asset class as they were in options or cryptocurrency trading.

Interactive Brokers has clearly figured out a winning formula to attracting new clients. Their platform and user experience, however, appeal to a narrower segment of users than something like Schwab or even Robinhood. What is undeniable, is that by creating a best-in-class product, maintaining a reputation for low-cost pricing and catering to the most influential user group in active trading, Interactive Brokers has shown that new clients will come.

Perhaps less obvious, Interactive Brokers has been playing a long game strategy.

Though they could not have foreseen a global pandemic tilting interest in their favour, their platform was nonetheless equipped to scale and did so when needed. They stuck to their strategy of focusing on their core segment (active traders) while recognizing the need to innovate (cryptocurrency, ESG investing, commission-free trading) to adapt to changing investor demands.

While it is difficult to extrapolate directly onto the Canadian online brokerage market, the key themes emerging from the latest Interactive Brokerage results, as well as the longer-term picture on account opening data across the big publicly traded online brokerages in the US, reaffirms that simply going commission-free doesn’t guarantee new account growth, nor does it guarantee loyalty.

That said, the pricing at Canadian online brokerages, for the most part, is very disconnected from the value offered.

Unless incumbent online brokerages are prepared to dramatically shift their development focus on delighting influential segments of self-directed investors, they should be prepared to significantly lower their commission pricing (or offer substantial sign-up bonuses).

When the new crop of online brokerages launches in Canada, COVID will be a fading memory and the conversation for most investors will be focused squarely on pricing and ease of use. As Interactive Brokers has shown, staying relevant is the best way to ensure you remain in the conversation, no matter where events in the world turn.

From the Forums

Heightened Coverage

When trusting an online brokerage with something as valuable as a nest egg, it’s important to know exactly what kind of assurances there are in place in case of a default. In this post from the investor forum on RedFlagDeals.com, one investor compares coverage available at two popular online brokerages and how vastly different the terms are.

Point of View

One of the latest features to emerge from Wealthsimple is a small but convenient improvement – a singular view of Wealthsimple Invest and Wealthsimple Trade accounts in one place. In this post revealing the new feature, users weigh in on the new view.

Into the Close

That’s a wrap on this edition of the Roundup. It was a bit delayed in going live, but perhaps we can chalk this one up to a chip shortage, the potato kind not the silicon kind (thanks Frito Lay). Besides, it seemed like there was more than enough to digest this week with market volatility keeping investors on edge. Here’s hoping for calmer waters and heads prevailing.

Unusual times are upon us. In the world of online brokerages, the beginning of March has historically been a turning point where RSP promotional offers expire, and the industry collectively takes a breath after their busiest stretch in the year. But this year, things are a bit different.

What unusual things that we’ve witness take place are an increase in cash back amounts from Qtrade Direct Investing coupled with extensions, again from Qtrade as well as RBC Direct Investing. And perhaps it is a sign of exactly how intense competition has become, but the RBC Direct Investing and Qtrade Direct Investing promos are at historic high levels. Another, for good measure, are longer deadlines for offers.

So, while we don’t have any new offers (yet) to report on, the extensions of offers from big names, like RBC Direct Investing and Qtrade Direct Investing, and longer durations of offers from Scotia iTRADE, would (or should) compel brokerages without an active promotion to consider launching an offer for the spring or through the summer.

In part, incumbent online brokerages – and especially bank-owned online brokerages – now need to factor into their promotional mix a world in which zero-commission trading from firms like National Bank Direct Brokerage (as well as Desjardins Online Brokerage) are gaining ground, and TD Easy Trade now exists. The new self-directed investor service from TD offers 50 commission-free trades per year to clients, and our recent in-depth analysis of TD Easy Trade shows why it is of immediate concern to competing brokerages.

Again, typically this would be a quieter time for all but a handful of perpetually active online brokers, but there’s a clear signal that in many ways these are not usual times, especially in the realm of self-directed investing. One possible reason: younger investors.

This new and materially relevant group of investors has started to drive all manner of change among online brokerages in Canada, which could mean that there are a few more interesting touchpoints in the calendar year where we see promotional campaigns surface.

For the time being, we’ll keep an eye out for new deals and promotions, but if you don’t see one on our list of online brokerage deals, let us know!

CIBC Investor’s Edge cash back promotion officially wrapped up on March 1st, as did the ultra-competitive cash back offer from TD Direct Investing. For reference, check out February’s deals and promotions post for a comparison of cash back promotions from the 2022 RRSP season.

Extended Online Brokerage Deals

RBC Direct Investing made a huge move this RRSP season by offering 100 commission-free trades which are good for up to two years. Originally slated to expire at the end of March, this RBC Direct Investing free trade promotion has now been extended to the end of November.

Another important extension was from Qtrade Direct Investing. In addition to revising the cash back bonus amounts upwards (and applying rewards retroactively to people who signed up under the original bonus), they also extended this offer until the end of April.

What a difference a few days makes. It’s hard not to pay attention to or be thinking about the tragic events unfolding in Ukraine. Despite there being many important turning points with the arrival of March, the one the world is focused on is the end of the conflict in Europe.

For online investors, this war has also shed light on the role that finance plays in the conduct of nations, including during conflicts. In particular, the steady drumbeats of war over the past few weeks have reintroduced uncertainty and volatility back into stock markets – something that could once again challenge online brokerage systems heading into the RRSP deadline.

In this edition of the Roundup, we put commission-free trading into the spotlight, in particular, the launch of a commission-free trading platform by TD. Also, we’re rebooting investor comments, which this week reflect the perennial question around low cost trading and the spillover of politics into choosing an online brokerage.

Easing into Commission-free Trading in Canada – TD Easy Trade

It’s no secret that Canadian self-directed investors are betting on the widespread deployment of commission-free trading among Canada’s discount brokerages. What investors may not have bargained for is what form that commission-free trading experience will take.

Just over a month ago, TD made an interesting move into the commission-free trading world by launching their “Easy Trade” app and offering up 50 commission-free trades per year on that platform. This new investing service replaces the TD GoalAssist platform (launched in 2019) and now offers yet another platform by TD for investors to execute trades on – albeit with limits.