Let’s call a spade a spade: things are in a terrible state. While we continue to watch from afar and hope that peace comes quickly to Ukraine, markets and investors closer to home are trying to digest world events having local consequences. And right now, we could all use something uplifting.

Fortunately, there are a few bright spots in this edition of the Weekly Roundup. To begin, we review the latest online brokerage deals and promotions, with a detailed look at how developments during the RRSP season portend what DIY investors can expect through the rest of the year. From there, we dive into a master class in continued growth by Interactive Brokers, whose latest metrics reveal that they’ve successfully navigated the new normal. Finally, tune into chatter from the investor forums to see what self-directed investors were focused on (other than oil prices).

Deals and Promotions: Rise of the Hybrids

While the holiday season is typically the time of year for gifts, it seems this year it was the RRSP season that gave self-directed investors the gift that keeps on giving: online brokerage deal extensions.

Things around the Canadian online brokerage industry are a bit unusual these days (see next story for more). Prior to the pandemic, there was a trend of online brokerages offering incentives and promotions that would typically start in November and last until the RRSP contribution deadline at the beginning of March the following year.

While last year was characterized by a tsunami of new investors clamoring to open online brokerage accounts, this year traffic is comparably quieter and thankfully more measured. And, despite crowd sizes returning to more manageable levels for online brokerages, the deals and promotions offered around RRSP season reflect a massive step change in the promotional landscape, driven in large part by increased competition and a whole new set of investors that are looking at trading online.

Before diving into the analysis of March’s deals and promotions reveal about the current competitive landscape, let’s begin with a recap of who’s in and who’s out.

A tale of two offers

The biggest promotions that expired at the beginning of March were from TD Direct Investing and CIBC Investor’s Edge. Both bank-owned brokerages, both cash back promotions.

What is interesting, however, is that on a year-over-year basis, the profile of the offer from CIBC Investor’s Edge was about the same, whereas for TD Direct Investing the minimum deposit requirement dropped 90%, from $15,000 to $1,500. Across multiple deposit tiers, TD Direct Investing also offered the highest (or was tied for highest) cash back amounts.

As small as this sample size is, it is illustrative of how Canadian online brokerages appeared to approach RRSP season this year.

On the one hand, there are firms that chose to stick to the traditional script, and on the other, firms that took a dramatically different route. Based on the numbers, it is clear that TD Direct Investing employed a different playbook, whereas CIBC Investor’s Edge stuck to their familiar game plan.

Perhaps it was the aggressive promotional approach of TD Direct Investing as well as the presence in the background of zero-commission trading at National Bank Direct Brokerage, Desjardins Online Brokerage, and Wealthsimple Trade that raised the stakes for online brokerage promotions during RRSP season.

That said, as the RRSP season went on, we witnessed three exceptional developments that suggest the current competitive landscape among Canadian online brokerages has shifted in a direction we believe is bullish for self-directed investors looking for a promotion when opening an online trading account.

A series of fortunate events

The first big shift in tactic came from Qtrade Direct Investing. At the outset of the RRSP season, Qtrade launched a cash back offer that looked like past offers. That is, they weren’t trying to be “first” when it came to cash back amounts.

That all changed in late January when Qtrade Direct Investing revised their cash back offering upwards and lowered the threshold to qualify for the promotions as well. They lowered their minimum deposit requirement from $15,000 to $5,000 and raised their minimum deposit bonus from $50 to $100. On a year over year basis, the revised Qtrade promotion was 80% lower for the minimum deposit threshold (from $25,000 down to $5,000) and two times higher in terms of minimum bonus. And it didn’t stop there.

Qtrade Direct Investing also raised their cash back amounts across numerous deposit tiers, matching the top bonus amounts in almost all of them. The only range where Qtrade Direct Investing was not tied for the highest cash back amount was in the $25,000 to $50,000 tier.

And this brings us to the second big development during the RRSP season, which is promotion extensions.

Historically, the expiry date of most online brokerage promotions would coincide with the end of the RRSP contribution season. This year, however, we saw expiry dates stretch out well beyond that point into March and April. And, as the RRSP season drew to a close, we started to notice deal extensions further into the calendar year.

For example, Qtrade’s cash back promotion now expires at the end of May (moved from an original expiry at the end of March). The RBC Direct Investing promotion, a fascinating development in its own right because of the number of commission-free trades (100) and term over which they can be used (two years), was originally scheduled to expire at the end of April and is now set to expire at the end of October. Joining this list of extensions is BMO InvestorLine, which has now extended its RRSP season cash back promotional offer into the end of May. Scotia iTrade has not extended their current offer (yet?), however, that is set to expire at the beginning of April.

Finally, another telling development during RRSP season this year was the launch of Easy Trade by TD. This new trading platform (which is separate from TD Direct Investing) offers 50 commission-free trades per year to its users. There is no doubt that when one of the largest banks in Canada launches a product that promises 50 commission-free trades per year, that self-directed investors (and other online brokerages) are going to pay attention. And, just in case they weren’t paying attention, TD heavily advertised the launch of Easy Trade during the Super Bowl and is continuing to advertise on social media as well.

Collectively, these developments are bullish for self-directed investors looking for better value (on commission pricing) and suggest that deals and promotions are going to fare more strategically into the approaches of online brokerages in the near term. In particular, those online brokerages that don’t want to drop their standard commission prices can, instead, launch a competitive commission-free trading promotion (as was the case with RBC Direct Investing). The events over this RRSP season also may serve as a harbinger of commission-free trading finally gaining widespread adoption in Canada.

Prior to the launch of full zero-commission trading at National Bank Direct Brokerage, this bank-owned brokerage offered 100 commission-free trades which were good for one year. Eventually, that promotion was superseded by the new pricing scheme. But in taking a measured approach towards zero-commission trading, it stands to reason that they could have reviewed the data associated with that promotion to decide about the impact of going to zero.

As TD showed with Easy Trade, zero-commission trading doesn’t necessarily mean full access to the suite of tools and capabilities that their TD Direct Investing online brokerage platform has.

It’s certainly a salient metaphor these days, but the “hybrid” option (aka unbundling) introduced by TD of paying for some trades or features and not for others could be how other online brokerages who currently charge for commissions approach the new world of zero-commission trading.

If other online brokerages follow suit, then just like at the pump, DIY investors looking for premium will be prepared to pay up. For everyone else, however, getting started with investing appears to be getting a lot cheaper.

Interactive Brokers: Numbers Reveal a Winning Formula

As we near the two-year anniversary of the official declaration of a global pandemic by the World Health Organization (March 11, 2020), the true impact of this once in a generation (hopefully) event is starting to become clearer. Although COVID is by no means behind us, almost anyone in the online brokerage industry can attest to how exceptionally different things are now than in the “before times.”

One area that probably doesn’t get much attention, however, is benchmarking. Specifically, how do you compare what’s taken place over the past two years to anything?

As it relates to online brokerages, be they Canadian or US, data from the past two years is showing that the changes to the industry have been profound. In many ways, not only is there a “new normal,” but new approaches are required and many of these are largely going to be written on the fly.

Earlier this month, as per usual, Interactive Brokers released their monthly performance metrics (for February 2022). Contextualizing these numbers, however, is particularly challenging because of how dramatically different the performance figures were in January and February of this year compared to last year. Though it may not be news that 2020 and 2021 were busy times – even by historic standards – what is particularly noteworthy is what you can see when net new account growth is plotted out back to 2019.

Because a picture is worth a thousand words, take a look at this graph of data of net new accounts at Interactive Brokers from 2019 to 2022.

Among the many things that jump out, it is striking to see the step change in interest in trading online that coincides with the start of the pandemic. Even more imposing is the surge in net new accounts in the first three months of 2021. Against that backdrop, the latest account growth figures reported by Interactive Brokers could be good, excellent, or terrible. Thankfully, context matters, and as such even though just under 39 thousand net new accounts represents a month over month decline in February of almost 22%, this still puts the strength of new account growth several times above where things were pre-pandemic.

Surges in interest aside, the longer-term picture points to a sustained interest – at least for Interactive Brokers – in trading online as indicated by net new account opens.

Prior to the pandemic, the average number of net new accounts in a month in 2019 was about 7.6 thousand. Excluding the period between January and March of 2021, the average between March 2020 and February 2022, the average number of net new accounts at Interactive Brokers has climbed to just shy of 38 thousand per month, a whopping 5x increase.

Focusing in on a more recent timeframe, it appears that the launch of cryptocurrency trading at Interactive Brokers in the late summer of last year helped to provide renewed enthusiasm for new account growth. Net new accounts opened in November 2021 (almost 55 thousand) reached the highest level seen since the end of the meme-stock craze in March.

Interactive Brokers’ continued account growth serves as a remarkable example of what is clearly a winning combination for active investors/traders.

Granted, some of the growth in their numbers is from acquisition. However, most new accounts have come through organic growth. Even more fascinating is that a material portion of their new clients have come to Interactive Brokers because of recommendations and referrals from existing clients.

Perhaps most remarkable of all, though, is that this data shows that growth can happen at an online brokerage that has a core business that charges commissions per trade, and against a backdrop where commission-free trading is the norm at many peer firms.

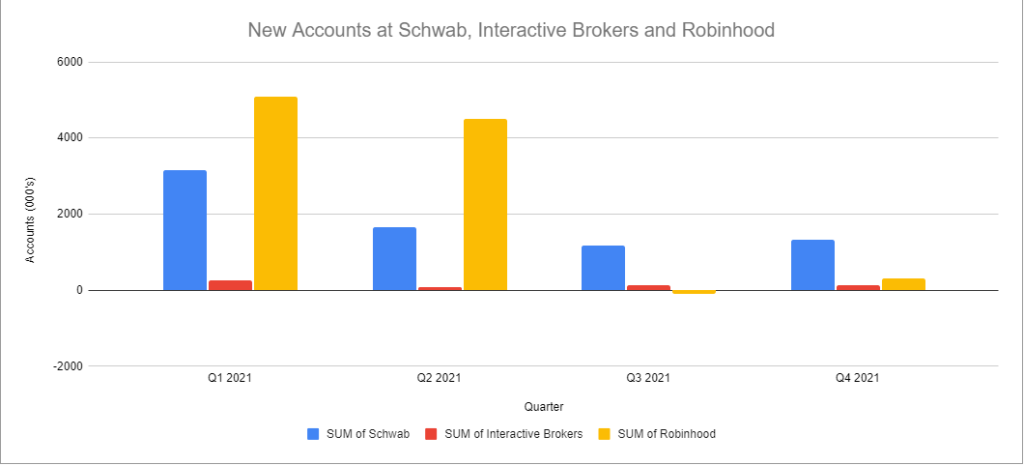

When comparing account growth figures across Interactive Brokers, Schwab, and Robinhood for 2021, it was revealing to see how poorly Robinhood fared against its peer firms in the back half of year – especially in the category of account openings. In contrast, Robinhood, which blew the doors off account growth in early 2021, saw a precipitous drop in account growth once meme-stock momentum faded.

As mentioned above, the truly exceptional nature of what happened in 2021 to the world of online investing makes comparing subsequent time periods against those first few months somewhat futile. The open question for online brokerages is whether the new entrants into the world of online investing are here to stay or simply a temporary phenomenon.

What the longer-term account data provided by Interactive Brokers suggests, however, there is more permanence to new users and continued interest in sophisticated platforms. Robinhood’s latest performance data has shown that especially when it comes to trading stocks, the new cohort of investors and traders were not nearly as interested in that asset class as they were in options or cryptocurrency trading.

Interactive Brokers has clearly figured out a winning formula to attracting new clients. Their platform and user experience, however, appeal to a narrower segment of users than something like Schwab or even Robinhood. What is undeniable, is that by creating a best-in-class product, maintaining a reputation for low-cost pricing and catering to the most influential user group in active trading, Interactive Brokers has shown that new clients will come.

Perhaps less obvious, Interactive Brokers has been playing a long game strategy.

Though they could not have foreseen a global pandemic tilting interest in their favour, their platform was nonetheless equipped to scale and did so when needed. They stuck to their strategy of focusing on their core segment (active traders) while recognizing the need to innovate (cryptocurrency, ESG investing, commission-free trading) to adapt to changing investor demands.

While it is difficult to extrapolate directly onto the Canadian online brokerage market, the key themes emerging from the latest Interactive Brokerage results, as well as the longer-term picture on account opening data across the big publicly traded online brokerages in the US, reaffirms that simply going commission-free doesn’t guarantee new account growth, nor does it guarantee loyalty.

That said, the pricing at Canadian online brokerages, for the most part, is very disconnected from the value offered.

Unless incumbent online brokerages are prepared to dramatically shift their development focus on delighting influential segments of self-directed investors, they should be prepared to significantly lower their commission pricing (or offer substantial sign-up bonuses).

When the new crop of online brokerages launches in Canada, COVID will be a fading memory and the conversation for most investors will be focused squarely on pricing and ease of use. As Interactive Brokers has shown, staying relevant is the best way to ensure you remain in the conversation, no matter where events in the world turn.

From the Forums

Heightened Coverage

When trusting an online brokerage with something as valuable as a nest egg, it’s important to know exactly what kind of assurances there are in place in case of a default. In this post from the investor forum on RedFlagDeals.com, one investor compares coverage available at two popular online brokerages and how vastly different the terms are.

Point of View

One of the latest features to emerge from Wealthsimple is a small but convenient improvement – a singular view of Wealthsimple Invest and Wealthsimple Trade accounts in one place. In this post revealing the new feature, users weigh in on the new view.

Into the Close

That’s a wrap on this edition of the Roundup. It was a bit delayed in going live, but perhaps we can chalk this one up to a chip shortage, the potato kind not the silicon kind (thanks Frito Lay). Besides, it seemed like there was more than enough to digest this week with market volatility keeping investors on edge. Here’s hoping for calmer waters and heads prevailing.